Writer: Varun Venkatesh | Editor: Sean Lu

Chinese President Xi Jinping might not be a fan of American rapper Kanye West, but even he could empathize with the sentiment behind “I miss the old Kanye”—or, in his case, the old China. Once a beacon of “flashing lights,” China’s economic glow has dimmed into a haze of uncertainty. As concerns mount, Beijing’s leading economists might be channeling Taylor Swift, wondering if “We Are Never Ever Getting Back Together” applies to the country’s former economic glory and current challenges.

A growing real estate crisis, declining consumer confidence and spending, and escalating international trade tensions are just some of the obstacles dimming China’s once-bright economic prospects.

China’s Property Market is a “Ghost Town”

China’s property sector, historically a cornerstone of its economic growth, is undergoing an unprecedented downturn. Indeed, in October of this year, new home prices across 70 major cities plunged by 0.5% from the previous month. That marks the 16th consecutive month of decreases and the largest year-on-year drop since 2015 of 5.9%. As a result, it is no surprise that investment in real estate has fallen by 10.3% from a year ago.

China’s economy structurally depends on investment, disproportionately accounting for 42% of the nation’s gross domestic product (GDP) of which 30% is controlled by the property sector. With such a large proportion of GDP dependent on the housing market, Beijing’s half-hands-on, half-hands-off involvement in property development has proven to be detrimental. The Chinese real estate crisis is a positive feedback loop, starting with property developers receiving and relying on extensive financing from the People’s Bank of China. Just recently, a $41 billion re-lending facility was established to provide low-interest financing to banks. Those banks then lend the money to state-owned enterprises (SOEs), who scale up subsidization to property developers to create more affordable housing.

However, after receiving financial subsidization, China’s largest property developers have free rein to leverage their assets without restrictions. Depending on bank loans to finance projects, developers have accrued trillions of dollars in debt, speeding up the creation of real estate but plummeting prices and spiraling debt out of control.

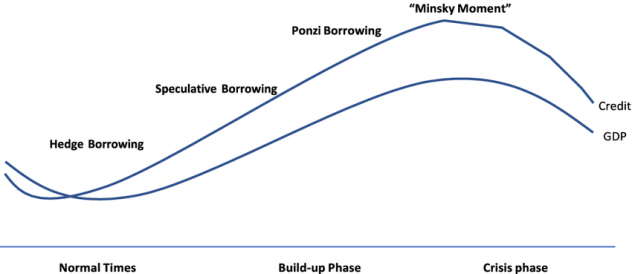

Economist Hyman Minsky’s financial instability hypothesis provides a framework for this occurrence. According to Minsky, extended periods of stability form the necessary conditions for extreme risk-taking, eventually causing financial crises. For China, the property sector was initially driven by rather sound investments; developers met their debt burdens through steady returns on completed projects. Consistently rising property prices reinforced the belief that real estate was a safe and profitable investment.

As optimism grew, Chinese developers began taking on riskier projects, relying on future price appreciation to cover the increasing levels of debt accrued from accepting bank loans. Debt repayment became dependent on the continuation of rising property values rather than the cash flow generated by the projects themselves.

Now, the system has reached a tipping point, the “Minsky Moment” (see Figure 1), where developers can no longer repay debts without borrowing even more. The assumption that property prices would continue to rise indefinitely failed to manifest in reality. Prices have fallen, unsustainable debt levels have been accumulated, and defaults have been triggered across the sector.

The housing market serves as a microcosm for the entirety of the Chinese economy, with consumers avoiding homeownership in an unstable property market in favor of liquid assets. This has led to a surge in precautionary savings, further depressing consumer spending. Indeed, homeownership rates among young Chinese adults dropped from 80% in 2018 to 64% in 2022.

Chinese Consumers Tell Xi: “You Can’t Tell Me Nothing”

Property struggles are supplemented by consumers’ dwindling confidence and diminishing spending, eroding another area of historical growth. Despite Xi’s establishment of financing programs that offer subsidies for spending, consumption is still not adjusting back to normal rates.

Consumers are shifting towards savings rather than continuing to discretionarily spend, fueling the economic slowdown. In 2022, household consumption expenditure decreased by 1.56%. Reductions in spending are reflected in broader consumer behavior; a November 2022 survey revealed that over 30% of respondents decreased spending on non-essential items compared to the previous year, with 43% cutting back on luxury goods. The decline in consumer confidence is further evidenced by the consumer confidence index dropping below 90 in April 2022, a record low. Events like the Singles’ Day shopping festival have seen lowered enthusiasm, reflecting a comprehensive trend of decreased consumer confidence.

With consumption down, producers are also missing economic benchmarks. The Purchasing Managers’ Index (PMI) for manufacturing fell to 49.5, down from 50.2 in September, signaling contraction as it dropped below the neutral 50 mark (see Figure 2).

“Power” Creates “Bad Blood”

China’s position as a geopolitical superpower serves as a double-edged sword for its economy. Times of crisis provide Xi the ability to further strengthen relations with allies; however, involvement in global conflict simultaneously worsens relations with affected acquaintances and competitor nations.

For instance, the U.S.-China trade war that began in 2018 saw the U.S. imposing tariffs on approximately $350 billion worth of Chinese imports, with China retaliating on $100 billion of U.S. exports. These measures greatly disrupted global supply chains and contributed to economic slowdowns in both nations.

Looking ahead, the re-election of Donald Trump raises concerns about a renewed trade conflict. Trump has proposed increasing tariffs on Chinese imports to 60%, a move that could severely impact China’s export-driven economy. Such tariffs could lead to significant revenue losses for Chinese exporters, further straining the global economy. China’s ability to redirect exports to other countries has already been limited due to rising global trade barriers, further complicating its economic strategy.

“Bound 2” Bounce Back

China has already tried conventional economic methods to stop its stagnant economy: increasing domestic investment, focusing on goods and services rather than physical capital and real estate, and cutting rates. Despite all of these attempts, projections estimate there would still exist a $142 billion shortfall in spending if Beijing is to meet its fiscal target for the year.

Stimulus in local areas, in the form of concerts, could serve as solvency for their problems. Ye’s recent ‘Vultures Listening Experience’ in China raked in over 50 million dollars of domestic tourism revenue. Taylor Swift’s ‘Eras’ Tour contributed an absurd 5 billion dollars directly to the global economy. Therefore, encouraging immersion in China’s performance industry could serve to improve China’s economic position and help to eliminate the current stagnation.

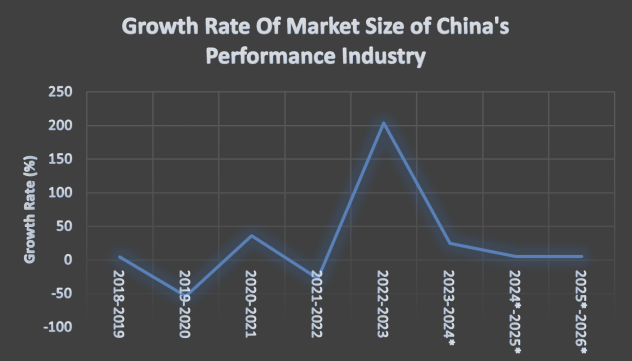

The market size of China’s performance industry fluctuated dramatically over recent years but saw immense growth between 2022 and 2023, where it surged by 203.74% (see Figure 3). This sharp increase reflects recent consumer interest in the entertainment and performance industry. The projections for 2024–2025 show continued, though more stable, growth rates (5.16% from 2024 to 2025), suggesting that concerts and performances, unlike previously relied upon economic areas, will become a reliable source of economic activity in the coming years.

Figure 3: Data Sourced from Statista

The Consumer Price Index (CPI) in April of 2023 for China also illustrates the importance of tourism and recreation, which saw a significant month-over-month increase of 4.6%, the highest among all categories by a definite margin (see Figure 4). This jump signals strong consumer spending in leisure activities, which includes attendance at concerts and live events.

Figure 4: Data Sourced from The National Bureau of Statistics of China

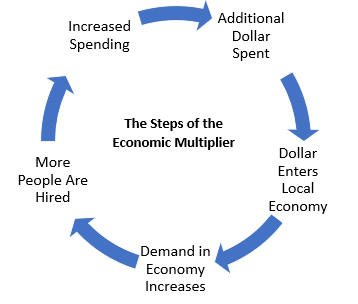

Recreational activities create a societal sentiment of normalcy, encouraging consumers to spend more freely. The performance industry’s distinct economic impact—the multiplier effect—is fueled by this increase in consumer confidence (see Figure 5). Direct, indirect, and induced spending in concerts and related industries triggers additional spending, expanding the overall economic impact.

As China faces increasing challenges, it’s clear the path forward requires Xi to “shake off” outdated strategies and embrace bold solutions. If successful, China could turn Ye’s “All Falls Down” into a “Homecoming” anthem, proving that even from the brink, its economy can rise again.

Assets for Featured Image from Rosa Rafael on Unsplash, Axel Antas-Bergkvist on Unsplash, and Maxim Hopman on Unsplash