ODYSSEUS PYRINIS – FEBRUARY 27TH, 2019

On March 2, 2017, Advanced Micro Devices (AMD) relaunched its efforts to retake market share from CPU giant, Intel Corporation. Zen, the new CPU architecture, was released by AMD to replace its inferior Bulldozer architecture. By increasing efficiency and performance, AMD contributed to what would become a battle between two silicon titans, AMD and Intel. As a result of this competition, consumers can benefit from advancements in computing performance and lower prices. What impact has this competition had on AMD and Intel? What does this mean for regular consumers?

AMD shocked the market with their brand-new Zen architecture in 2017, a new line of Ryzen CPUs, budget processors for the regular consumer, and Ryzen Threadripper CPUs, high performance processors for PC enthusiasts and content creators. Intel was uniquely challenged for the first time after over a decade of commanding market dominance. While similar in performance to Intel processors, AMD processors were sold at a fraction of the price.

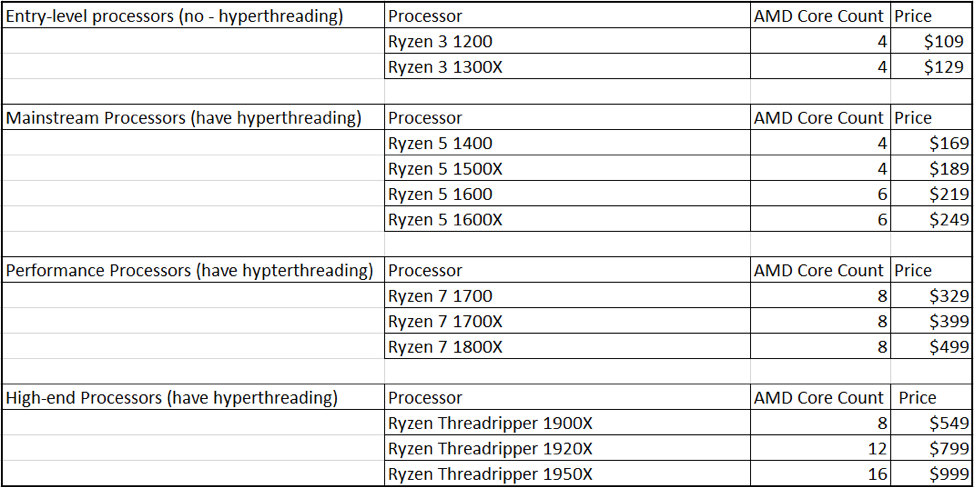

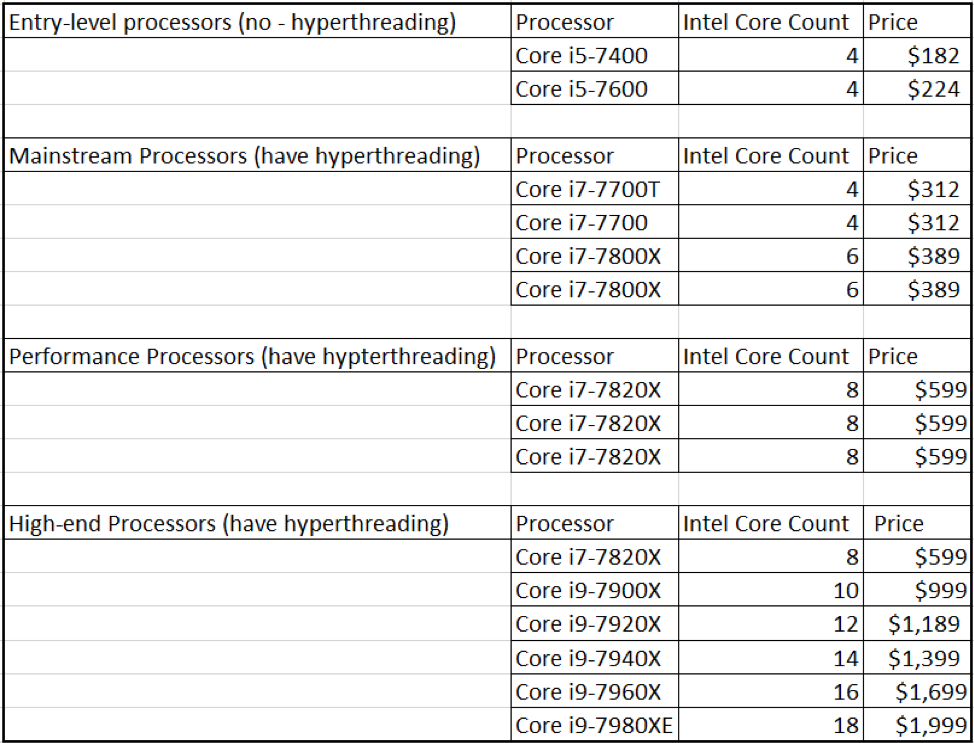

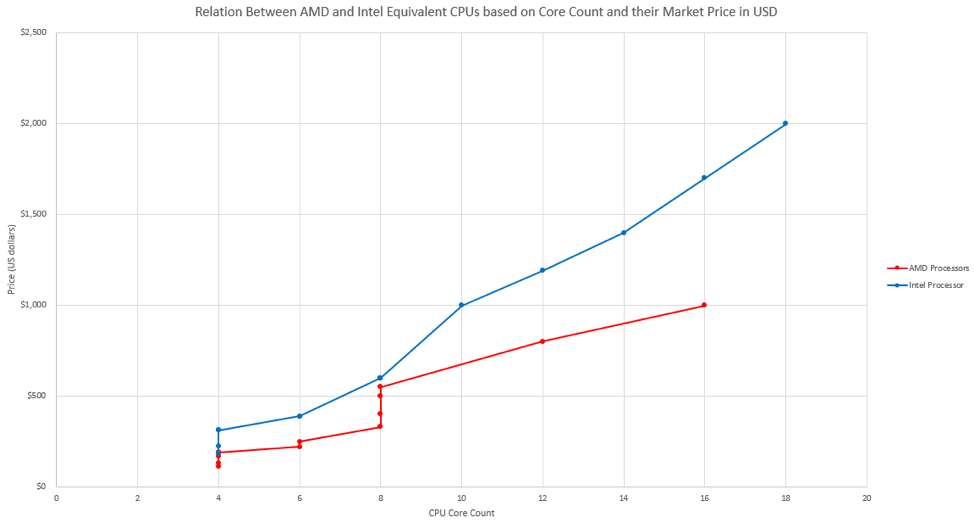

There are numerous factors that affect performance including: core count, core frequency, amount of level 1, level 2 and level 3 cache, CPU architecture, and the type of tasks run on the CPU. To demonstrate the price disparity between Intel and AMD processors in 2017, core count will be used to measure similar performance among processors that have similar base and boost frequencies. The tables also identify those processors that do and do not include hyper-threading technology.

As indicated by the figure, AMD strategically priced their new line of processors to be more affordable than Intel’s equivalent offerings. There is a large price gap between AMDs high computing performance CPUs and their Intel equivalents. This suggests that AMD is targeting both the consumer and producer markets with an emphasis on transitioning content creators and studios to its new Ryzen platform. For mainstream consumers, AMDs offerings are very compelling: why would you pay $312 for an i7-7700 with only four cores when you can pay just $17 more and get a Ryzen 7 1700 with double the core count translating to greater multi-thread performance?

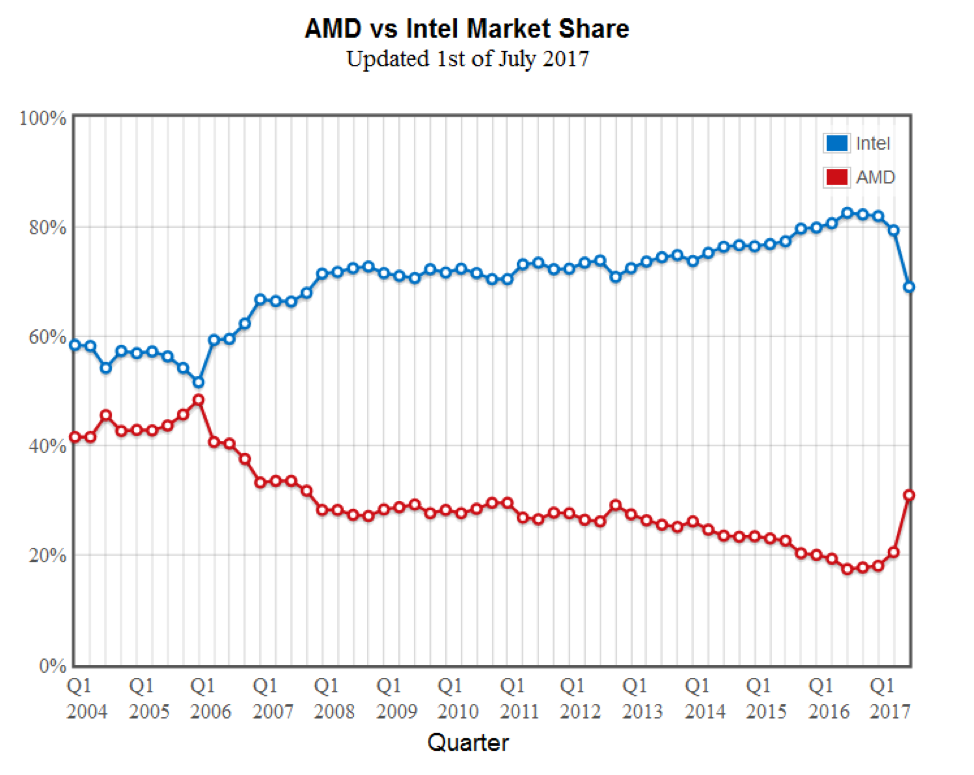

Given the pricing of these processors, AMD was expected to dominate the CPU market and steal the majority of Intel’s market share, but results have suggested otherwise. An estimation of the new market share acquired by AMD on the consumer processors can be derived from PassMark’s benchmark submissions. It is important to note that PassMark can only provide an approximation since it counts the number of active systems using the service rather than the number of systems sold with the respective hardware. PassMark also only includes any systems that run Windows. Nevertheless, AMD’s gains in market share are noticeable and significant. In quarter 4 of 2016, Intel commanded 81.9% of the consumer CPU market, while AMD represented a measly 18.1%. The tables turned shortly after the launch of the new Zen architecture, unscathed by Intel’s counter-launch of its new Kaby Lake series processors. Intel’s market share dropped to 69%, while AMD’s rose to 31% of consumer systems. The historical record of Intel and AMD’s market share is depicted in the figure below.

The general trend is apparent: prior to 2017, Intel saw a gradual increase in their market share while AMD suffered great losses and even considered terminating production of their CPUs. This changed after the launch of the Zen architecture in 2017.

Before AMD’s introduction of Zen, it appeared as if the market had reached a period of stagnation with regards to technological innovation. Dual core processors and quad core processors were the mainstream for years, but that all changed after AMD’s breakthrough in the market. In the last two years, consumer processors have advanced from quad core CPUs to 28 and 32 core CPUs. The slated release of new manufacturing techniques, such as AMD’s new 7nm manufacturing process, have also been accelerated to outpace their competitor.

Consumers have been the primary beneficiary from both Intel and AMD to outpace the other’s performance and value of CPU offerings. Consumers are now able to acquire significantly greater performance for a fraction of the cost, thus increasing the value of the processor. With a decrease in price, more consumers are deciding it is time to buy, whether it’s a pre-built system or if they must assemble the computer themselves.

Due to greater consumption of CPUs, Intel has been facing a shortage in processor supply. Intel and AMD utilize different CPU sockets. Since the price of a new motherboard can be a significant cost to building a system, it is very common that when consumers decide to upgrade their CPU, they do not upgrade the motherboard. This means that consumers with an AMD socket on their motherboard can only upgrade to a new AMD processor that supports that socket. The same is true for Intel CPU sockets. This has driven third party vendors to increase the manufacturer’s suggested retail price (MSRP) of Intel’s processors. Meanwhile, AMD’s price remains low, allowing them to carve into Intel’s market share, which will also affect the long-term market share.

However, despite AMD’s enticing offerings, Intel did not lose the market share to AMD that had previously been estimated. Perhaps it is because of Intel’s brand name as a dominant player in the CPU market with a well-established reputation for reliability and computational performance, something that AMD did not have until 2017. Furthermore, Intel has remained on a single monolithic die, which means that all cores on the die are interconnected into a single integrated circuit. AMD has been able to increase their core count on their processors by taking a different approach. For example, on AMD’s 32-core Threadripper variant, only 16 of the cores are on a monolithic die, or have direct access to memory and Peripheral Component Interconnect Express (PCIe) lanes. The other 16 cores communicate with the initial 16 cores using a proprietary technology called Infinity Fabric. This design results in half of the cores in the CPU to be strictly computing cores, relying on the other half of the cores to provide them with information from RAM.

The advantage of AMD’s approach is that they can easily expand the core count of their CPUs in the future. This allows AMD to increase parallel computing performance at an unprecedented rate. Intel’s monolithic die design does not allow for such scaling, at least not as easily. AMD’s approach also results in lower CPU costs. The fabrication process of a CPU die is extremely complex with numerous stages where even a slight error can render the final product inoperable. With a monolithic die, the higher the core count, the more expensive it is to manufacture due to non-functional cores that result from fabrication errors. AMD instead relies on interconnecting multiple lower core count CPUs to form a higher core count CPU. AMD’s new 32 core Threadripper CPU, for example, is really four of AMD’s eight core CPUs that are interconnected using Infinity Fabric. A lower core count CPU is more tolerant to fabrication error resulting in lower individual CPU costs.

In the new competitive climate in the CPU market, both Intel and AMD have attempted to keep themselves one step ahead of the other, pushing the boundaries of what is computationally possible. With AMD’s patented production process for scaling the core count of their CPUs and Intel’s pressing threat of a CPU shortage, Intel has decided to invest another $1 billion in production facilities to minimize their shortage and increase supply as much as possible.

The current CPU market features high value offerings from both companies. Intel still holds the title for best single threaded performance; however, AMD has provided significant competition with respect to multi-threaded performance. In AMD’s attempt to acquire greater market share and Intel’s efforts to maintain their current market share, the value of CPUs has increased significantly from previous generations delivering greater performance for a fraction of the cost. In the interim, advancements in processing technology and architecture have been accelerated. The primary beneficiaries of this heated competition are without a doubt the consumers, who are now able to access the performance previously reserved for datacenters and corporations with multi-million-dollar technology budgets.

Featured Image Source: Technology X

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.