GRACE JANG – NOVEMBER 20TH, 2019 EDITOR: GILLIAN SERO DEL MUNDO

Background

This month, the Organization of Economic Cooperation and Development (OECD) called for a global minimum corporate tax rate to curb large multinationals’ tax avoidance. This proposal is part of the OECD’s larger program of tax reform to ensure a fairer allocation of taxing rights. Since its initiation last month, the OECD has introduced plans to allow countries to “tax back” if other jurisdictions have offered extremely low tax rates and tax operations that have no physical presence in their jurisdiction. These measures overall are intended to prevent multinational corporations from shifting profits to low- or no-tax jurisdictions to minimize their tax payments and to discourage countries from lowering tax rates to attract those businesses. However, they would be particularly damaging to technology and pharmaceutical multinationals, among others, that derive substantial profits from intangible assets like patents and brand.

This move by the OECD gained momentum following France and Britain’s implementation of unilateral digital tax schemes and several other European countries revealing plans to introduce similar measures. The French tax was especially controversial for supposedly discriminating against big US technology companies, specifically online advertising platforms like Google and Facebook and intermediary service providers like Uber and Airbnb. The opposition from US tech giants subsided only after France assented that it would eliminate the tax once a new international agreement on digital taxation is reached. Previous negotiations at the level of the European Union (EU) and the OECD have failed in reaching a consensus; in fact, the new tax reform of the OECD is just the latest development in the international attempt to find a common tax regime on digital sales, for which tech companies pay less than half of the effective tax rate applying to physical bricks-and-mortar firms in the EU.

It is widely believed that companies owning intangible assets often avoid paying taxes in countries where they make significant sales by declaring their profits in tax havens or registering their offices there. Intangible assets do not have significant physical presence in any one location, so it is possible for companies owning intangible assets to artificially locate their sources in tax havens. For example, even if a tech company is based in the US and raises a sizeable revenue in France, it could declare its profit in Ireland because its digital operations have no physical presence in any one of these countries. Additionally, there is a high chance that the company would do so to pay less tax, since Ireland has a much lower tax rate than the US or France. In fact, our analysis below suggests that the largest US tech companies like Apple and Microsoft do engage in this kind of practice.

Even though a wide range of industries base their operations on intangible assets, many global tax policies are centered around online technology sectors as seen in the recent tax schemes of the European states and the OECD. This is quite understandable — just considering the US companies, tech giants are predominantly the largest players in the global market, and along with pharmaceutical companies, they have the most cash parked in offshore subsidies. Given the importance of US tech giants in both the worldwide economy and cash spread, a question that naturally comes to one’s mind is, “How do US tech companies relate to the global corporate tax structure, and to what extent is this relationship characterized by tax avoidance?” In our study, we seek to answer this question by examining the tendency of US tech giants to locate their foreign subsidiaries in tax havens and comparing it with case studies on Chevron and Boeing, representing energy and industrial sectors respectively.

Methodology

Out of the 25 US companies with the largest global market capitalization in the year 2019, we have identified tech companies based on their sector and sub-industry, as classified by the Global Industry Classification Standard (GICS). We define tech companies mainly as those in the Information Technology or Communication Services sector, but also consider the sub-industry and nature of business of each company. For example, we define Amazon.com Inc. as a tech company despite its GICS classification as a Consumer Discretionary sector, because it mostly runs online operations as implied by its Internet & Direct Marketing Retail sub-industry classification. Furthermore, we exclude Cisco, which is classified as an Information Technology sector and Communications Equipment sub-industry, because its business requires a physical location and reach to customers. In the end, we have 11 tech companies, in addition to Chevron and Boeing, to be further analyzed.

Next, we obtain each company’s list of subsidiaries and their locations from the most recent 10-K filings submitted to the US Securities and Exchange Commission (SEC). It is worth noting, however, that the SEC recently started allowing companies to only list their principal subsidiaries, so the 10-K filings’ lists of subsidiaries most likely leave out dozens or hundreds more. The problem is further complicated by the stringent confidentiality rules in most offshore jurisdictions. This renders it extremely difficult to gather information on offshore subsidiaries, even once the existence of the unreported subsidiaries is known. Nonetheless, given that this is a common, if not unavoidable, problem facing research related to tax havens, we move on with our study using the SEC’s 10-K filings as our source.

We then rank jurisdictions based on their tax haven scores for the year of 2019; the Tax Justice Network only publishes information about the top 64 jurisdictions with the highest Corporate Tax Haven Index (CTHI). Accordingly, we categorize worldwide jurisdictions into six brackets: Quantile 1 to Quantile 5 each comprises of 12 jurisdictions from the order of the highest to the lowest tax haven scores; the group called “Others” consists of all the other countries and territories that do not fall under Q1 to Q5. Then, for each of the 13 companies in question, we assign each foreign subsidiary owned by the company to a single bracket based on its location and count the number of foreign subsidiaries in each of the six brackets. Finally, we obtain the percentage of foreign subsidiaries in each bracket for the total of the 11 tech companies, as well as the percentage statistics for Chevron and Boeing.

Result

The following analysis provides a visual summary and explanation on the percentage statistics of the technology sector, Chevron, and Boeing.

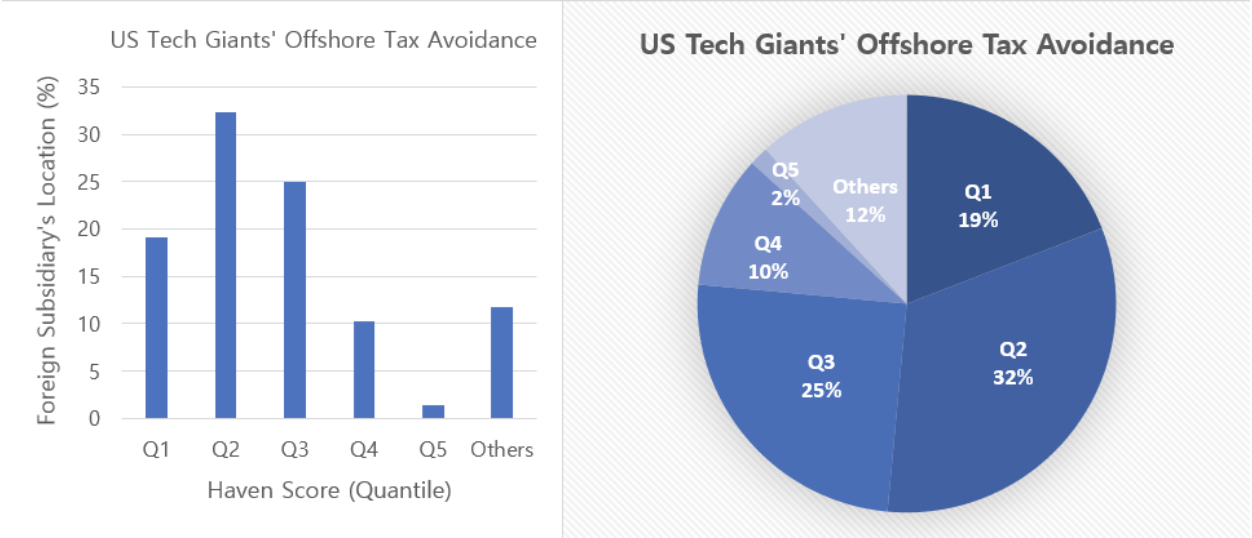

Figure 2 shows that US tech giants tend to locate their subsidiaries in tax havens; the percentage of subsidiaries shows a decreasing pattern from the more tax-lenient jurisdictions to the less lenient, except for Quantile 1 and Others. Considering that there are a total of 195 countries in the world, which puts at least 135 jurisdictions into Others, the percentage of subsidiaries located in Others is minimal and suggests that US tech players prefer to register their foreign subsidiaries in a relatively small number of offshore financial centers over most other parts of the world.

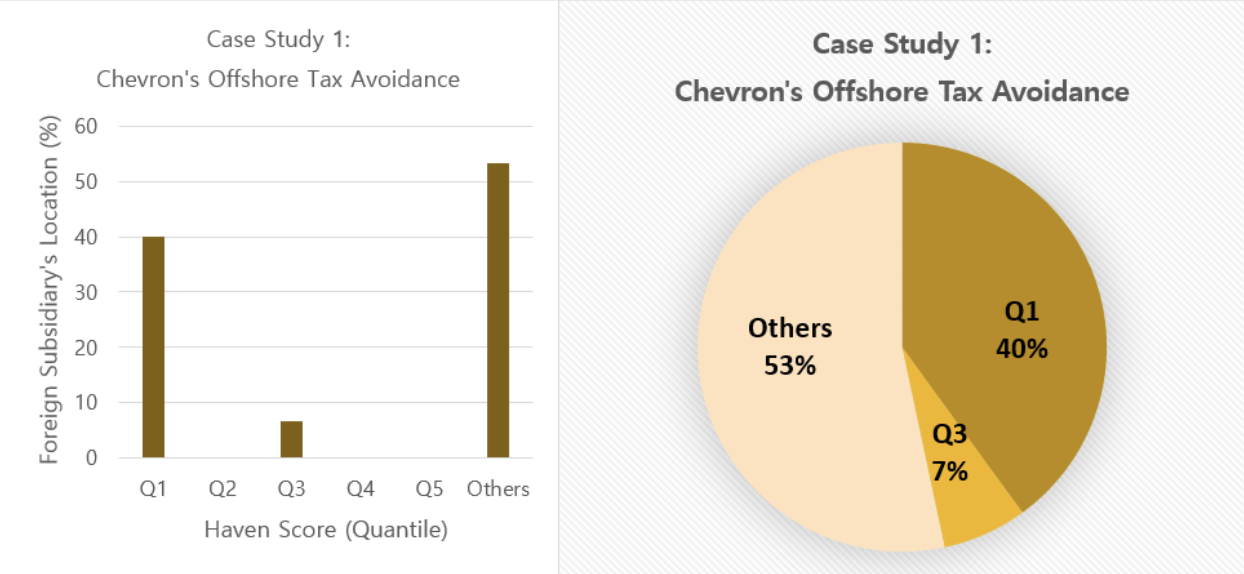

Regarding Chevron, six out of fifteen foreign subsidiaries are in the Bahamas and Bermuda of Quantile 1, and eight are in countries like Argentina, Australia, Canada, and Nigeria of Others. These locations reflect both the physical bases of Chevron’s oil and gas operations (Latin America, Australia, West Africa, and North America are the largest regional bases of its energy exploration and production) and its effort to pay less tax through strategic positioning of subsidiaries in the world’s most important tax havens.

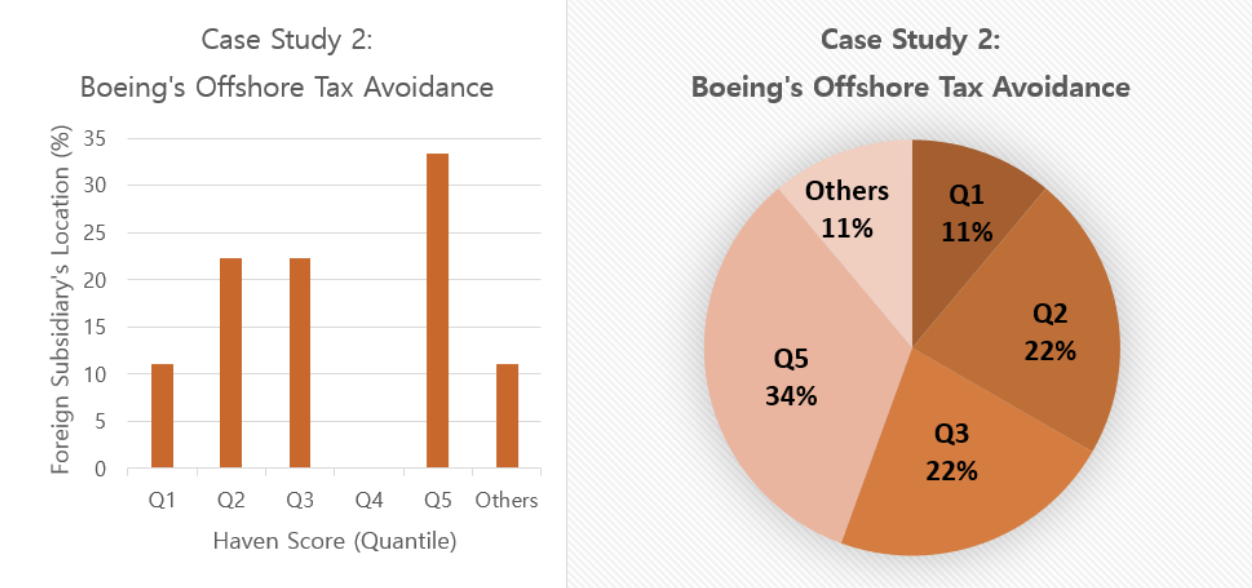

As for Boeing, its arrangement of foreign subsidiaries mirrors the significant weight that the company gives to physical location and epitomizes the geographic distribution of foreign subsidiaries common in heavy industry. Boeing’s foreign subsidiaries show an increasing level of concentration from the most tax-indulgent Quantile 1 to the most tax-stringent Quantile 5, with more than half of them in Germany and the UK, which harbor Boeing’s key manufacturing facilities. This may be because the physical nature of its main operations requires its headquarters’ location to correspond to the actual sites of operation, however high the tax rates may be in those sites. Thus, this result suggests that companies like Boeing which primarily engage in offline activities are less likely to practice offshore tax avoidance than companies that rely predominantly on electronic commerce, again reinforcing the argument that cyberspace presents at once opportunities for tax avoidance and challenges for cross-border tax regulation.

Conclusion

On the whole, the leading US tech companies practice more offshore tax avoidance than do the traditional bricks-and-mortar businesses, exemplified by Chevron in the energy sector and Boeing in the industrial sector. The top 11 US tech corporations place their principal foreign subsidiaries in a few tax havens rather than in other jurisdictions that compose a majority of the countries worldwide. Our results substantiate the allegations made by non-US countries that US tech giants register their subsidiaries in offshore financial centers, taking advantage of the online nature of their businesses to avoid the high tax rates of countries that they raise large revenue from. In this respect, the OECD’s overhaul of its century-old tax regime is long overdue and ever more important. It remains to be seen whether the new international tax framework would effectively adjust to the changing character of global economy without excessively compromising the corporate growth.

Featured Image Source: CNN

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.

But I’m never going to stop telling you something about your post. Your job. Nothing I can tell you about your post. You do outstanding job