NICOLAS DUSSAUX – APRIL 21ST, 2020

EDITORS: JENNIFER JACKSON, PARMITA DAS

Are financial institutions now leading the real economy rather than the opposite? Although some pundits seem to still differentiate the immaterial financial flows from the “real economy,” the recent impact of the COVID-19 outbreak on financial markets shows firsthand the two-way interactions between the markets and supply chains. Even before the epidemic, the heightened tensions in the Middle East led to a decrease in the valuation of Saudi Aramco, the famous Saudi Arabian oil company that went public during the fall. Another process that perfectly illustrates the predominant role of financial institutions in the “real economy” is common ownership. Common horizontal ownership (or shareholding) is the simultaneous possession, by institutional investors, of shares in several companies that compete against each other. As the goal of these funds is to optimize the returns on their portfolio, a very concerning contradiction arises between the interest of the fund and the self-interest of the company. Indeed, regulators are concerned about whether common shareholding undermines the competitiveness of markets, which can directly translate into an increase in prices. It is a topic that is still widely debated within academia, with some scholars dubious of claims that common ownership has any impact on the economic structure of markets and prices.

How can Common Ownership undermine competitiveness?

As outlined in a previous article, there are various ways to assess the competitiveness of markets, some more commonly used and relevant than others. We can try to assess competitiveness by comparing levels of prices and output in a market and looking at the way these metrics behave through regression analysis or correlation matrices. Another way to assess the competitiveness of a market is by looking at the concentration of the market, using indicators such as the Herfindahl-Hirschman Index (HHI) that assesses the concentration of a market on a value from 0 to 10000.

HHI = ∑ (% shares of companies)2

For example, a market split evenly between two companies would yield HHI = 5000. The HHI has been widely used by the Federal Trade Commission (FTC) in Mergers and Acquisitions cases. This model relies on the assumption that each firm acts independently and tries to maximize its own profit. However, scholars make the case that when an institutional investor owns shares in more than one company in the same market, we see a rise in prices and a decrease in the incentive to innovate, which harms consumers in the long run.

If we look at the airline industry, we realize that the four major carriers in the United States are partly owned by BlackRock, Vanguard, Fidelity, Berkshire Hathaway and State Street. Further, at United Continental Airlines, only 5 of the top 100 owners do not hold shares in another of the top four.

Indeed, asset management funds optimize at the portfolio level, leading to a push for companies to internalize any externalities inflicted on their competitors, rather than a push for the management of individual companies to maximize profits. This creates a fundamental conflict: while the funds seek to reduce aggressive competition in markets to increase industry profits as a whole, the management of these companies are hesitant to forego the profits of their individual companies. According to Einer Elhauge, a professor at Harvard Law School, it is less relevant to look at the direct interactions between management and mutual funds and more relevant to look at the incentives common ownership creates for the management of these companies. The managers are pushed to maximize the profits of their shareholders in an effort to gain their support, which means adopting practices that reinforce the industry as a whole.

These practices are not illegal in the same way that collusion is. It is very important to understand that the argument made by the funds, which is that they are not asking their firms to collude, has little to do with the problem. In fact, as Martin Schmalz, economics professor at University of Michigan outlined, collusion is a means of profit maximization that generally arises to maintain anti-competitive outcomes when there are incentives to compete and constant communication between the management of both companies. In this case, common ownership simply reduces incentives to compete and, thereby, leads to the same outcomes as collusion. Therefore, a relationship between management and the funds is not even required, as profit incentives are enough to initiate such a dynamic in the industry.

Clearly, it is a legitimate question to ask how exactly investment funds engage in undermining competitiveness. Although Elhauge thinks that the negative effects of common ownership can occur independently from investors’ actions, Martin Schmalz claims that the inefficiencies induced by common ownership result from a deliberate strategy used by the investors to reduce competition. They take advantage of the legal tools at their disposal, their votes and their voice, to avoid prosecution by regulators.

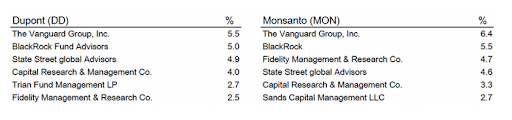

In a note posted on Eric Posner’s (law professor at the University of Chicago) website, Schmalz argues that the financial press wrongly interpreted a proxy fight between the hedge fund Trian and the current management of Du Pont de Nemours, one of the largest agrochemical companies in the US. Trian is the fifth largest investor of DuPont. In a filing to the SEC, Trian described how their bid would have improved the performance of DuPont by splitting their activity, aggressively increasing Research and Development, and ceasing some practices that Trian called “too lenient” towards competition. For instance, DuPont had paid an additional $750 million settlement to Monsanto and, soon after, engaged in a licensing agreement that would (according to Trian) “cost too much” for DuPont. In short, Trian was advocating to replace the management by accusing them of providing too little growth to the company. Surprisingly, Trian lost the fight and went down in history instead as an activist fund that had tried to dismantle a successful company.

The fact that Trian lost their bid is not surprising, especially considering the fact that an increase in DuPont’s competitiveness would have directly harmed its main competitor, Monsanto. Indeed, a closer look at the shares of Monsanto reveals that the leading investors in the two companies are the same.

In line with Schmalz’ argument, BlackRock, Vanguard and State Street all voted against Trian’s proposal, resulting in the activist fund losing its bid. Consequently, DuPont’s stock price incurred a sharp drop, letting commentators believe that financial markets shared Trian’s concerns. DuPont’s inability to cut costs served the direct interest of the funds. The same funds kept the joint profits of Monsanto and DuPont high, significantly harming competition in the market.

After a roundtable, the European Commission concluded that common shareholding could have long-lasting negative impacts on incentives to innovate. In fact, mutual funds are rarely willing to forego profits in the short run by investing in Research and Development. In a competitive market, investing in R&D is absolutely necessary in order to avoid being driven out of the market by a more innovative competitor. However, in small markets where ownership is controlled by a small number of firms, such incentives fade.

Common ownership has become an increasingly widespread phenomenon. According to Einer Erlaughe, the probability that two large competing firms have a large horizontal shareholder increased from 16% in 1999 to 90% in 2014. However, most regulatory authorities do not consider the economic evidence provided by research as sufficient to edict strict rules regarding common ownership. Professors such as Erlaughe have made several proposals, such as utilizing a modified HHI that could better evaluate the structure of markets, but the modification suffers from some methodological flaws and is still debated in academia.

Similar to most anti-competitive practices, common ownership is directly harming the consumer. This issue calls for a more careful assessment of the markets by regulatory authorities and a closer look at the practices of the largest investors.

Featured Image Source: CoinRevolution

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.