SANIYA PENDHARKAR – APRIL 26TH, 2024

EDITOR: ESMA OZGUN

Since the aftermath of World War II, over one hundred countries have participated in a currency union, defined as the adoption of a single currency amongst a group of nations. While the most famous and oft-cited of these is the European Union, other active unions include the West African Currency Union, which uses the CFA Franc, and the Eastern Caribbean Currency Union, which operates on the Eastern Caribbean Dollar.

Theoretically, monetary unions should increase the volume of trade by reducing transaction costs. They mitigate risks of financial loss due to exchange-rate fluctuations and standardize business regulations, all of which should hypothetically facilitate cross-border investment. Nevertheless, there has been extensive scholarly debate about the magnitude of these benefits and the size of their influence on trade, with the European Union serving as a prominent case study.

The European Union (EU) consists of approximately thirty countries, operating as a single market in order to allow the trade of goods, services, and capital. The Economic and Monetary Union (EMU) is a subset of the EU that involves the coordination of economic and monetary policies between member countries. The main goal of the EMU is to attain economic stability and integration via the adoption of a common currency, which is the Euro. The EMU is further governed by the European Central Bank (ECB), which is responsible for the policies in the Eurozone, such as a single market policy or the Common Agricultural Policy, both of which maintain the goal of achieving ideal and equitable trade throughout the union.

So, let’s address the underlying question: while currency unions should, in theory, increase the flow of goods and services due to the practical benefits they promise to member countries, how much of an impact do they actually have on trade?

The Gravity Equation: All for One and One For All?

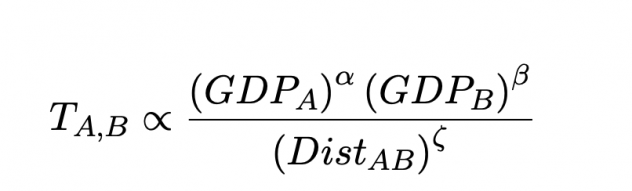

Researcher Andrew Rose pioneered the literature surrounding this question by utilizing the standard gravity model framework with a basic currency binary variable as a right-hand regressor. In economics, a gravity model predicts bilateral trade flows (the exchange of goods between two countries aimed at enhancing investment and trade connectivity) based on the size of the economies and the physical distance between the two countries.

Image source: NBER Working Paper Series

Figure 1: The gravity equation where A and B represent countries in a pair. T is the trade flow, Dist is the distance between countries, GDP represents the economic dimensions of the countries, and α, β, ζ ≈ 1.

The gravity model illustrates that, with regards to the level of bilateral trade, the distance between two countries is inversely proportional whilst the size of their economies is proportional. Rose’s methodology not only accounts for the geographical distance between countries and the magnitude of their economies, but also includes an additional variable that indicates whether or not countries share a common currency.

Image source: Oxford Research Encyclopedia of Economics and Finance

Figure 2: Shows the log scale of the relation between the distance between countries and the costs of trade. The line of best fit indicates that for every 1% increase in distance, there is a corresponding decrease in trade by 1.4%.

Rose’s regression provided predictable results: countries with higher GDP had greater levels of trade, and countries further from each other had lower levels of trade. These predicted conclusions aside, one incredible estimation was that countries who shared a common currency experienced a three-fold increase in trade when compared to countries with differing currencies! Even holding all other variables constant in the model (i.e. common language, colonial ancestry, trade organizations, etc.), countries that shared a currency exhibited greater volumes of trade, supporting the conclusion that currency unions do, in fact, significantly benefit trade.

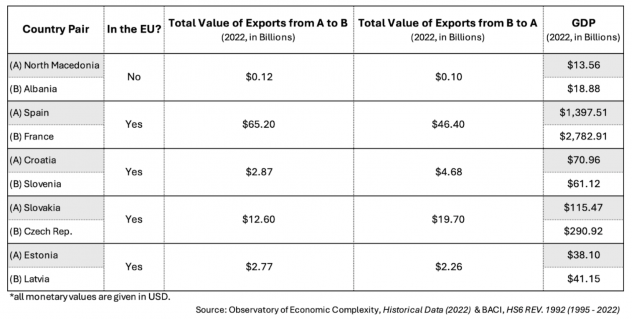

One drawback of this model is that the framework produces only a single coefficient to assess the effect of trade. This means that the result is assumed to be homogenous across all pairs of countries analyzed in the gravity model (i.e. the three-fold increase in trade was estimated for all pairs), which, of course, cannot be accurate since there are unique variables for each pair of countries that must be considered. This can be easily proven with basic export data from The Observatory of Economic Complexity.

Image source: The Observatory of Economic Complexity

Figure 3: Comparing export values of country pairs not in the EU with country pairs in the EU. The distance between each pair is constant (each pair represents bordering states), and the GDPs are comparable. GDPs sourced from Macrotrends | The Long-Term Perspective on Markets

An examination of Figure 3 demonstrates that bilateral trade among bordering countries within the European Union is more than threefold that of bordering nations outside. However, there is considerable variation between the EU pairs themselves. For instance, the export value from Spain to France is over 543 times greater than that from North Macedonia to Albania. Similarly, the export value from Croatia to Slovenia is nearly 24 times that between North Macedonia and Albania. These disparities suggest that Rose’s assumption of a homogeneous coefficient is not universally valid. Of course, this example is incredibly oversimplified, as it does not take into account other factors, such as inter-country relations and economic histories, and the table showcases only one non-EU pair. Despite these limitations, the data presented in the table does showcase the variation in bilateral trade within the EU and therefore challenges Rose’s estimated coefficient.

A one-size-fits-all value is impractical given the multitude of factors affecting the trade dynamics between two countries. Subsequent literature highlighted the need to control for additional determinants of bilateral trade, such as the relative level of trade barriers or unobservable factors that are country and time-specific. Taking these considerations into account, and assuming symmetry between entries and exits of currency unions, more recent literature has concluded more modest estimates using the gravity model, ranging between statistically significant figures of 4.3% and 6.3%, on average.

Overall, no matter which two EU countries are compared, one will find that their trade systematically surpasses that of countries not in the union. If this is the case, the question still remains — why aren’t there more currency unions? Can the success of the EU be replicated in other regions?

South America – An Unattainable Union?

As aforementioned, outside of the Euro exists the CFA Franc in Africa and The Eastern Caribbean Currency Union; even Asia could form a union in the future in an attempt to reduce reliance on the dollar. What about the prospect of a South American union? If anything, one can argue that the similarities between these countries are comparable if not greater than those of European countries: they share a similar colonial history, overlapping languages, and similar distributions of GDP (akin to Africa, which has two unions). Given these conditions, the gravity model discussed earlier should be successfully applicable. What, then, explains the absence of a union?

There have been talks of an El Sur currency (translating to “the South”) primarily led by Argentina and Brazil, with both presidents declaring that “Nothing is more emancipating than the fraternity of nations.” The reality is that Latin America, despite shared commonalities, is economically fragmented, with only 15% of trade occurring within the region compared to 55% for Europe. Latin America also faces a host of challenges, ranging from political instability to fiscal discipline, casting doubt on central bank credibility and hindering the viability of a currency union.

Image source: World Economic Forum

Figure 4: Argentine and Brazilian Presidents talk at a summit of the Community of Latin American and Caribbean States; both parties noted that a common currency will not be instilled.

For example, the collapse of the Argentine Peso against the US dollar in 2018 sent the country into an economic crisis, causing it to consistently boast the world’s highest inflation rates in the last few years (rising to a shocking 211.4% in early 2023). Not unlike Argentina, Venezuela has also been a victim of hyperinflation that has rendered the country’s currency practically useless. On the other hand, economies like Uruguay and Chile have been relatively stable. A currency union would thus have unequal benefits for prospective members, likely helping to stabilize Argentina and Venezuela, but with unclear effects for steadier nations. Indeed, in contrast to the more evenly distributed trade in Europe, Latin American trade is concentrated in only a few countries. Argentina, Chile, Brazil, and Venezuela account for more than fifty percent of all exports. Similarly, these four countries consume almost fifty percent of all imports. Once again, we find ourselves asking: where is the common benefit?

In the absence of a common benefit for member countries, the emergence of a currency union is infeasible. Moreover, the benefits associated with a union are not a panacea for pre-existing economic grievances, as they require strong institutional prerequisites, social support, and political will. Thus, to establish a successful monetary union, there must be political motivation, economic stability, and fiscal health.

Closing Remarks

After analyzing the data and claims of Andrew Rose and other notable scholars, it is evident that currency unions do have a positive impact on trade by allowing for increased economic exchange between participating nations — though quantifying the actual effect that unions have on trade is more difficult and subject to debate. Additionally, the viability of a monetary union depends on a number of factors, one being the economic capacity and political will of prospective member countries. Regardless, there is a significant influence of currency unions on the volume of trade, so despite existing obstacles, it is likely that more countries will advocate for currency unions in the future.

Featured Image Source: WorldAtlas

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.