SANIYA PENDHARKAR – NOVEMBER 15TH, 2023

EDITOR: ANGELA CHEN

The housing problems that have affected the United States for years are nothing short of a square off between supply and demand: decreasing supply is worsened by an increasing demand. A large hindrance to the supply side of the real estate market is its declining elasticity. In economics, elasticity of supply refers to responsiveness of the quantity supplied to a change in the price. With a lower elasticity of supply, the amount of available housing is not greatly influenced by prices. It also means that house prices are more sensitive to demand. The huge housing boom in 2012 has many common trends to the one of the late 90s; however, while demand and prices increased during both periods, supply did not in 2012, and today, supply continues to stagnate.

Additionally, supply is impacted by interest rates. When the economy experiences inflation, the Federal Reserve increases interest rates in order to counter it. This increase leads to high mortgage rates, making monthly payments less affordable. Thus, current homeowners are less likely to sell since they are content with their low mortgage of the past.

Furthermore, this has also led to a greater gap in housing inequality. With rents rising, it has become harder for lower income tenants to afford them. As a result, higher income people have replaced such residents, resulting in a significant decrease in vacancies, further lowering supply. Additionally, while homeownership is the American Dream, homeownership rates have increased slower than rent since 2006, as low supply and high interest rates have made this option unattainable for lower income populations.

With the aftermath of the Great Recession, the COVID-19 pandemic, and foreign strife, high inflation rates have maintained this loop of decreased supply and increased demand.

In The Beginning: The Great Recession

In the 1980s, America experienced the crushing weight of high mortgage rates. The record high 20% mortgage rate of the oh so “Glorious Eighties” destroyed the real estate market like nothing before. However, only twenty years later, banks started laying the groundwork for a similarly disastrous subprime crisis, ultimately leading to the 2006 housing market collapse, the 2007 global financial crisis, and the Great Recession.

The Great Recession is strongly argued to be caused by the Great Financial Crisis, which began with the boom in the housing market. The American economy was doing well for itself as the new century approached, and the housing market was experiencing its normal fluctuations. But in 2001, the number of single family homes climbed and climbed…and climbed. The turn of the century brought along a great demand for houses and companies were constructing homes with fervor. Those with poor credit histories and high debt- to- income ratios were offered subprime mortgages. With banks eager to take advantage of the instantaneous money flowing in, they approved subprime mortgages left and right with no consideration of long term effects.

This didn’t seem too bad at first since interest rates were on the decline from 1996-1998; however, as the 2000s approached, interest rates increased by as much as 33%. To make matters worse, the practices of selling mortgage backed securities (MBS) to domestic or foreign investors paired with credit default swaps—where an investor purchases an MBS at a premium and pays the MBS value plus interest in case of a default—became prevalent. Investors from all over the globe were in a frenzy over these subprime securities. They poured money into the US real estate industry expecting to make hefty returns. Many were successful at first, cashing in on millions of American dollars, but when subprime mortgages inevitably began to default, investors started losing money.

Graph Source: The Evolution of the Subprime Mortgage Market

As a result, rates of debt negligence grew at an exponential rate from 2006 until they peaked at just under 11.5% in 2010. As the chaos worsened, countless defaults and foreclosures led to a crash in the US housing market. Meanwhile, foreign investors also lost incredible amounts of money, leading to a domino effect in other countries and the ultimate downfall of global banks like Lehman Brothers.

In the aftermath of this great shock, many Americans lost their homes. Those who were able to keep their homes faced financial catastrophe as their home value tanked and interest rates climbed. In many cases, mortgage payers willingly defaulted on their loans because it was better than paying for their now depreciated home which required doubled mortgage costs. As a result, homebuilding companies froze and supply sank: an effect America has not recovered from decades later.

A large number of regulatory changes also went into effect. The Federal Reserve cut the federal funds rate to zero—something we also saw during the COVID-19 pandemic—in order to encourage economic growth. The Fed also decided to lower interest rates to allow people to access capital and reinvest, but people were not quick to trust low rates nor invest.

When the World Shut Down and Finally Woke Up: The COVID-19 Pandemic

The second cause of the American housing crisis was the pandemic. What started out as a two week break from work and school soon became two and a half years of isolation, restrictions, and significant changes. The Coronavirius pandemic caused disaster in every department, from health to agriculture, to the economy and even housing. Economic fears were already widespread before the pandemic, but with the world shut down and the markets on pause, the problem became much worse.

In addition to the individual lockdown rules, mass layoffs and business failures weren’t keeping anybody’s hopes up. Everything was unpredictable and people were scared. The importance of having cash on hand and maintaining financial security in the early months trumped any desire of purchasing hard assets like a house.

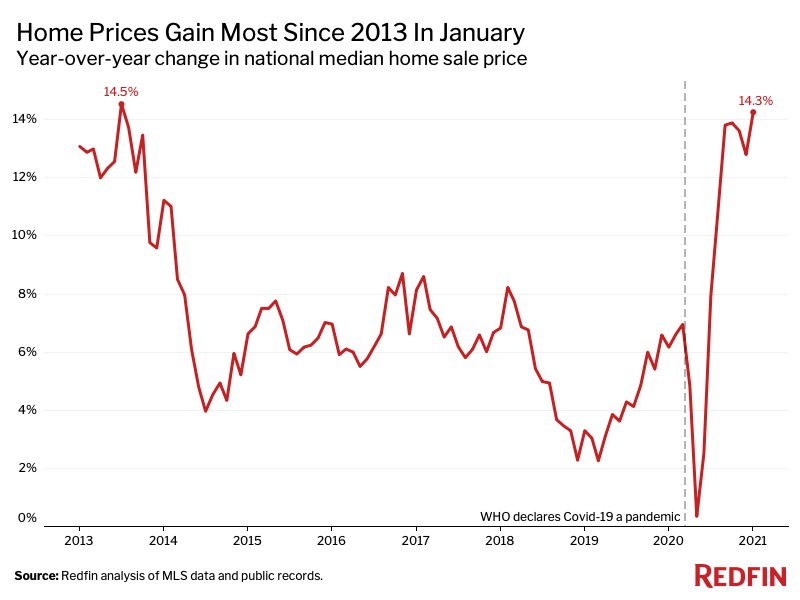

However, as post-pandemic life began to bloom once again, economic growth followed an upward pattern, and people found themselves with an excess of savings from years of stay-home policies. This led consumer spending to follow an upwards trajectory and has ultimately led to a huge boom in housing demand. However, after the steep decline in housing construction from the Great Recession and the pandemic, housing was in short supply.

Graph source: Redfin

Other factors also worsened the shortage. With restrictions easing and families slow to leave the security of their homes, people began home renovation projects. The huge increase in demand for renovation projects along with decreased global production caused lumber prices to triple between 2020 and 2021. This also affected the long run supply of homes because renovations allowed people to add the backyard pool or home theater they’ve always wanted, making it less likely that they will move and further lowering the supply of homes.

Another factor to note is the relocation of corporations. Firms were able to relocate to states with lower operating and land costs without having to worry about laying off or finding new workers. For example, Tesla’s plan of constructing a headquarter and other Elon Musk operations have moved to Texas. Other large companies like Apple and Google have also found new homes in Texas thanks to its abundance of acreage and cheaper land costs, especially when compared to the companies’ previous California offices. While this has been great for the corporate side, this boom has had a huge effect on the demand for Texas homes, causing a state once applauded for low housing costs to experience incredible price increases in the span of a couple years.

The pandemic has undoubtedly affected all Americans, but those in the lower income quartile have been affected the most. Regions with greater financial vulnerability experienced greater Covid-19 deaths and infections; Pew Research Center recorded that 33% of people living in these areas lost their jobs or wages due to the pandemic, compared to just 14% of the upper quartile.

Polarizing Politics: Bidenomics

In recent years, Bidenomics and government policy has been, to no surprise, an incredibly polarizing topic in the United States. Greater government involvement, regulation, and taxation have characterized Biden’s term. Biden’s proposed seven trillion dollar budget for fiscal year 2024 was largely fueled by an increase in taxation, as opposed to cuts on government spending. However, increased taxation would never be enough to finance such a large budget, so Biden additionally approved $4.8 trillion of borrowing which has led the Federal Reserve to create trillions of dollars to finance this large-scale borrowing.

Okay, but what about housing? Well this large scale borrowing had a predictable outcome: inflation, which has certainly hurt the housing market. In order to cool off inflation, the Federal Reserve raised interest rates and crunched credit. With greater interest rates making it difficult to finance anything, consumers have experienced complications as both median rents and mortgage payments have risen.

Mortgage rates are high, but they are not nearly as high as the record breaking 20% that the early 1980s saw. So, why is the housing problem now just as big? The primary difference is that a much greater fraction of an American’s take-home pay is going towards financing a mortgage because for decades home prices have increased at a faster rate than incomes. Another problem lies in those who were able to buy a home before Bidenomics took charge. These people are now tethered to their own homes; they cannot sell because home prices are too high and they would lose their current and much more attractive mortgage rates. This has crippled the supply side. The drop in the housing supply continues to put upward force on housing prices, while increased government spending continues to pull interest rates up.

Since Biden has become president, there has been a 27% increase in median home prices and a 5% increase in interest rates; both of these factors have raised the mortgage of a median priced home by roughly $1000 annually.

The Biden Administration has fortunately not turned its cheek on the housing issue plaguing America. In 2022, Biden announced the Housing Supply Action Plan, which aims to close the housing supply gap in five years and ease the burden of housing costs over time.

As the name reflects, Biden believes the best thing to be done in order to ease the burden of housing costs is to increase the supply of quality housing. While this includes building new homes, it also means preserving old ones—this ensures that the new units do not simply replace the old ones. An independent analysis done by NOVOGRADAC on these proposals found that they could finance about 1 million homes (certainly helping the 1.5 million shortage). The plan also aims to provide incentives for land use and zoning reform, as well as limits to regulatory barriers. Furthermore, by leveraging transportation funding from the Bipartisan Infrastructure Law, the administration hopes to encourage state and local governments to increase the supply of housing.

Concluding Remarks

The Great Recession, COVID-19 Pandemic, and Bidenomics have each substantially affected America’s housing market. The disparity between supply and demand has escalated due to interest rates, stark changes in lifestyle, and new government policies. However, despite this disparity, a full fledged housing crash is extremely unlikely since housing prices have been recovering, and in some places steady since June. But, as housing fears still persist, confidence in the American housing economy will be slow to grow.

Featured Image Source: Archpaper

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.

{kind=link}

{kind=link}