ALLY MINTZER – FEBRUARY 26TH, 2020

EDITORS: JENNIFER JACKSON, PARMITA DAS

Unemployment is at 3.6% (a near all-time low) and GDP is at $21.73 trillion (a record high), while the stock market continues to break records. As GDP continues to rise and the stock market continues to break records, it seems the economy is doing well. However, these statistics, hailed by politicians and the media alike, do not convey the full message of the state of our economy.

The unemployment rate does not tell us what type of jobs people have, if they make a living wage, or the number of jobs they must hold to support themselves. GDP does not tell us how equally distributed goods and services are throughout a population and, more importantly, where and with whom the benefits of such economic growth are being realized. Moreover, the stock market figures do not tell us which US socioeconomic or demographic groups are benefitting from these highs. Behind the astounding facts of low unemployment, a booming GDP, and a successful stock market, is the alarming truth of wealth inequality.

Before examining the history of wealth inequality, it is first important to define what wealth is. In a nutshell, wealth is “assets minus liabilities.” For many families, “assets” consist of savings, real estate, 401(k) retirement plans, while “liabilities” are composed of mortgages, student loans, and credit card debt. Wealth differs from income, which is defined as the salary one makes in a year from wages, interest, and capital gains before tax deductions. Income is a way for families to “get by,” while the accumulation of wealth enables families to advance their economic situation. Although there is a significant overlap between the wealthiest 1% and the top 1% highest income earners, there are many who do not fall in either category. Furthermore, although income inequality is serious, wealth inequality is more consequential.

Wealth inequality is not a new phenomenon. Given the capitalistic premises of America’s current economic system, a certain degree of wealth inequality is inevitable. Wealth inequality has persisted throughout our country’s history, albeit to varying extents. For instance, in the “Roaring Twenties,” industrial titans dominated the American economy. The decade witnessed the three richest people ever to have existed—John D. Rockefeller, Andrew Carnegie, and Cornelius Vanderbilt—who were worth a combined $890 billion in today’s dollars.

After the crash of the Great Depression in 1929 and the Second World War that followed, a series of progressive policies caused wealth inequality to subside. As part of the New Deal, marginal taxation was increased, social services were expanded, regulations rose, and unions were strengthened. In the 1950s, the top marginal tax rate for incomes over $200,000 ($2 million in today’s dollars) was above 90%; however, it is contested whether the rich really did pay these taxes. In the 1960s, tax loopholes closed as marginal rates fell (with the top marginal tax rate being 70%), and Medicare and Medicaid were created as a means of providing public healthcare. In the 1970s, the Earned Income Tax Credit for working families with children earning less than $41,000 to $56,000 was enacted. By the 1970s, the Gini Coefficient—a metric used to describe the distribution of income in a country, in which a lower digit implies more equality—was in the low 30s.

However, by the 1980s, a series of neoliberal economic policies from President Ronald Reagan, nicknamed “Reaganomics,” began to unravel the economic policies attempting to limit inequality. Reaganomics was based on the Laffer Curve, which promised that lowering taxes would lead to higher tax revenue and tax cuts at the top would “trickle down” to the rest of America. Taxes were slashed and regulations unfurled. The Gini Coefficient has risen ever since.

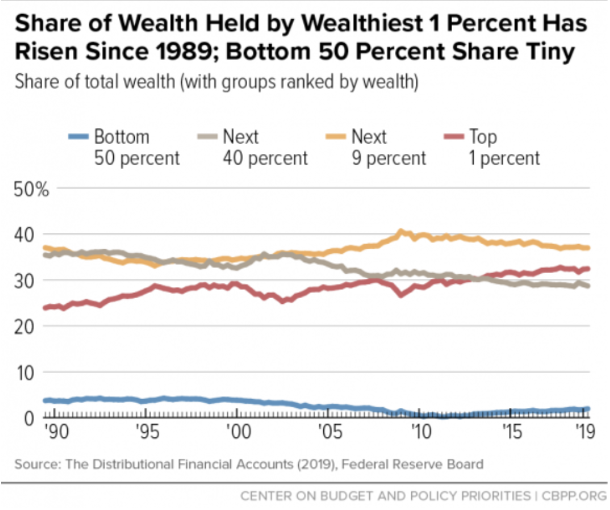

Today, wealth inequality is returning to the level of the 1920s, and is currently three times as high as it was in 1970, begging the question: how bad is wealth inequality today? According to the most recent report from the Federal Reserve’s Survey of Consumer Finances, since 1980, the wealth held by the top 1% rose from 30% in 1980 to 39% in 2016. By contrast, wealth held by the bottom 90% fell from 33% to 23%. UC Berkeley economists Emmanuel Saez and Gabriel Zucman report that the share of total wealth of the top 0.1% (about 160,000 families who have net assets of $20 million and above) increased from 7% in 1979 to 22% in 2012, a level comparable to the 1920s.

As such, the average real wealth growth rate of 1.9% per year from 1986 to 2012 is not equally distributed across economic classes. Saez and Zucman conclude that the wealth of the top 0.1% has grown 5.3%, as their capital allows them to save more and take advantage of capital gains. The wealth of the bottom 90% has not grown proportionally due to stagnated wages, fall in savings, and surges in mortgage, consumer, and student loan debt.

The type of wealth also varies across percentiles. For 90% of Americans, most of their wealth comes from their home (which, of course, was the asset hit hardest during the 2007-2008 Recession). On the contrary, most of the wealth of the top 1% is accumulated through stocks and mutual funds. According to the Federal Reserve’s Distributional Financial Accounts, the top 1% own more than half of the wealth invested in stocks and mutual funds.

Racial inequalities also factor into wealth disparities. In 2016, the average (defined as the 50th percentile) white family was worth $163,000 and had 10 times the wealth of the average black family (at $16,000) and 7.5 times the wealth of the average hispanic family (at $22,000). The same racial wealth disparities continue to exist even when accounting for similar levels of higher education. In 2016, the Federal Reserve Bank of St. Louis reported that for every $1 in wealth a white, college-educated family had, a black college-educated family had $0.17 in wealth and a Hispanic family had $0.19. By contrast, in the 1990s, these numbers were $0.31 and $0.34 respectively.

Our nation’s epidemic of wealth inequality presents dire effects for the working and middle classes. Many can not afford the universal right of healthcare, the egregiously high costs of higher education, or simply earn a living wage. According to the OECD, the average increase of inequality of 3 Gini percentage points decreases GDP by 8.5% as poorer families cannot invest in education.

Just as jurist Louis Brandeis noted, “We may have a democracy, or we may have wealth concentrated in the hands of the few, but we can not have both.” Wealth inequality subsequently creates an imbalance of political power, especially when the rich use their wealth to fund their own political campaigns, donate money to PACs which support like-minded candidates, or lobby for policies that serve their own interests, which are often antithetical to the interest of the general public. For example, as Vanderbilt University professor Larry Bartels asserts, only 40% of the wealthy support a minimum wage high enough to ensure that a full-time worker can keep his or her family above the poverty line, while 78% of the general public support this policy. As economic insecurity increases, so does scapegoating; under the current presidential administration, racism, xenophobia, and islamophobia have become more blatant. Violent hate crimes have reached a 16-year high, with notable increases in hate crimes targeting Latino, transgender, gender-noncomforming, and Sikh people.

As Stanford University historian Walter Scheidel notes in his book, “The Great Leveler,” history has shown that extreme wealth inequality has led to several dire outcomes: revolution, war, plague, or state collapse. The last time period of extreme wealth inequality saw the crash of the stock market and the onset of the Great Depression. At that time, 1 in 4 people were unemployed and almost half of the banks failed. This led to reforms such as the creation of financial regulations and institutions like the Federal Deposit Insurance Corporation and the Securities Exchange Commission.

However, it would be excessively dogmatic to assume that wealth inequality can be solved simply; it is evident there is no “quick fix” to wealth inequality. Globalization presents unique opportunities for tax avoidance, political polarization hinders our ability to come to a consensus, and it is unclear whether technological advances will augment or mitigate inequality. Perhaps, to begin to restore the fundamental rights of life, liberty, and the pursuit of happiness for all, we must ask ourselves whether we can defend the laws that allow for the accumulation of wealth in the hands of the few at the expense of the many.

Featured Image Source: Humor Times

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.