JONATHAN LI – NOVEMBER 9TH, 2021

EDITOR: DIVYA VEMULAPALLI

I. The Impact of COVID on small-businesses

On March 11, 2020, the World Health Organization declared COVID-19 as a global pandemic, resulting in a crashing economy with millions facing unemployment. To provide financial relief, the Federal Government released a wave of stimulus checks to cushion the economic impact on households. Recently, with the development of vaccines, the economy is beginning to reemerge from its slumber, with aggregate demand and inflation rates rapidly rising. To match the sudden burst of consumer demand, businesses are scrambling to raise production through obtaining capital, raw materials, and workers.

During the pandemic, low-skilled workers began shifting their views on employment, with 66% of the unemployed “seriously considering” finding higher-paying fields of work. One possible explanation behind this trend is that heighted unemployment benefits decreased the cost of leisure, allowing workers to raise their standards for employment. Hence, a combination of unemployment benefits and shifting workforce attitudes have led to workers holding out for higher wages, resulting in 10 million active job openings in the US: the highest in US history. Consequently, 41% of small businesses are experiencing rapid wage cost increases and struggling to compete against large corporations that have greater flexibility to boost wages and benefits. To compound the crisis, 70% of small businesses are also experiencing rapid increases in supply costs from national shortages. Thus, even after the peak of the pandemic, many small businesses continue to either struggle with costs or shut down due to this new economic climate.

II. The Implications of Small Business Performance on the Macroeconomy

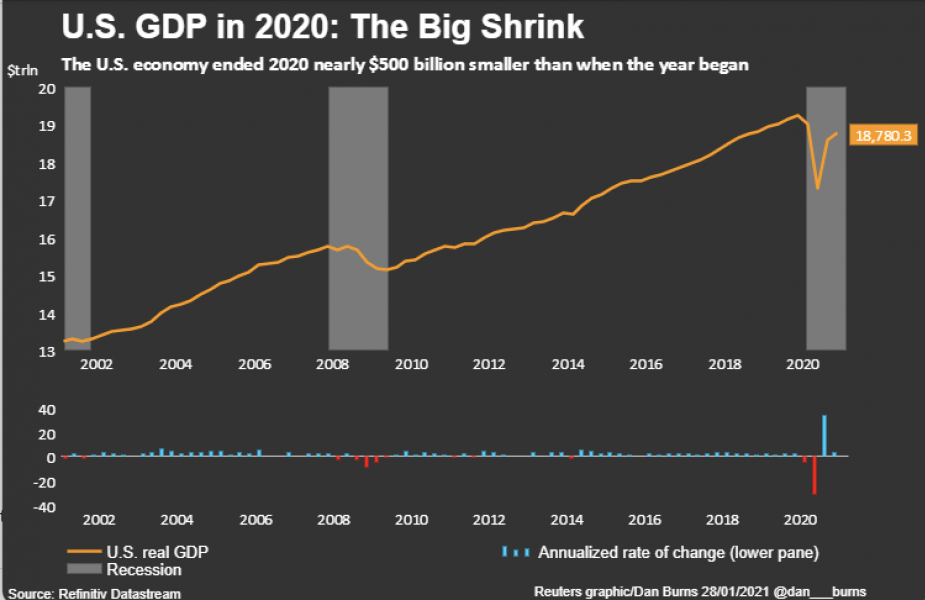

The shut down of small businesses has calamitous effects on US real output. In the US economy, small businesses generate two-thirds of net new jobs and account for 44% of US economic activity and GDP, yet a Federal Reserve report finds that the first year of the pandemic resulted in the closure of an additional 200,000 small businesses from average historic levels. Illustrated in the figure below, US GDP decreased by 3.5% – the largest drop since 1946 – and consumer spending, which accounts for two-thirds of aggregate demand, dipped by 3.9% during 2020. In the road to recovery, increasing the presence of small businesses will be vital, given their role in consumer spending and output.

Even if small businesses don’t entirely shut down, their rising prices in response to labor and supply shortages have long-lasting implications on national inflation rates. In July 2021, US inflation rates reached 5.4%, a massive spike relative to pre-pandemic rates. Importantly, higher inflation is likely not a temporary blip and is here to stay over the next several years, given the Fed’s new framework surrounding inflation. In an August 2020 speech at the Jackson Hole conference, Federal Reserve chairman Jerome Powell announced that the Fed will keep interest rates low “until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2% and is on track to moderately exceed 2% for some time”. In essence, the Fed – which had previously aimed for a maximum inflation rate of 2% – is now aiming for an average inflation rate of 2% over the long run.

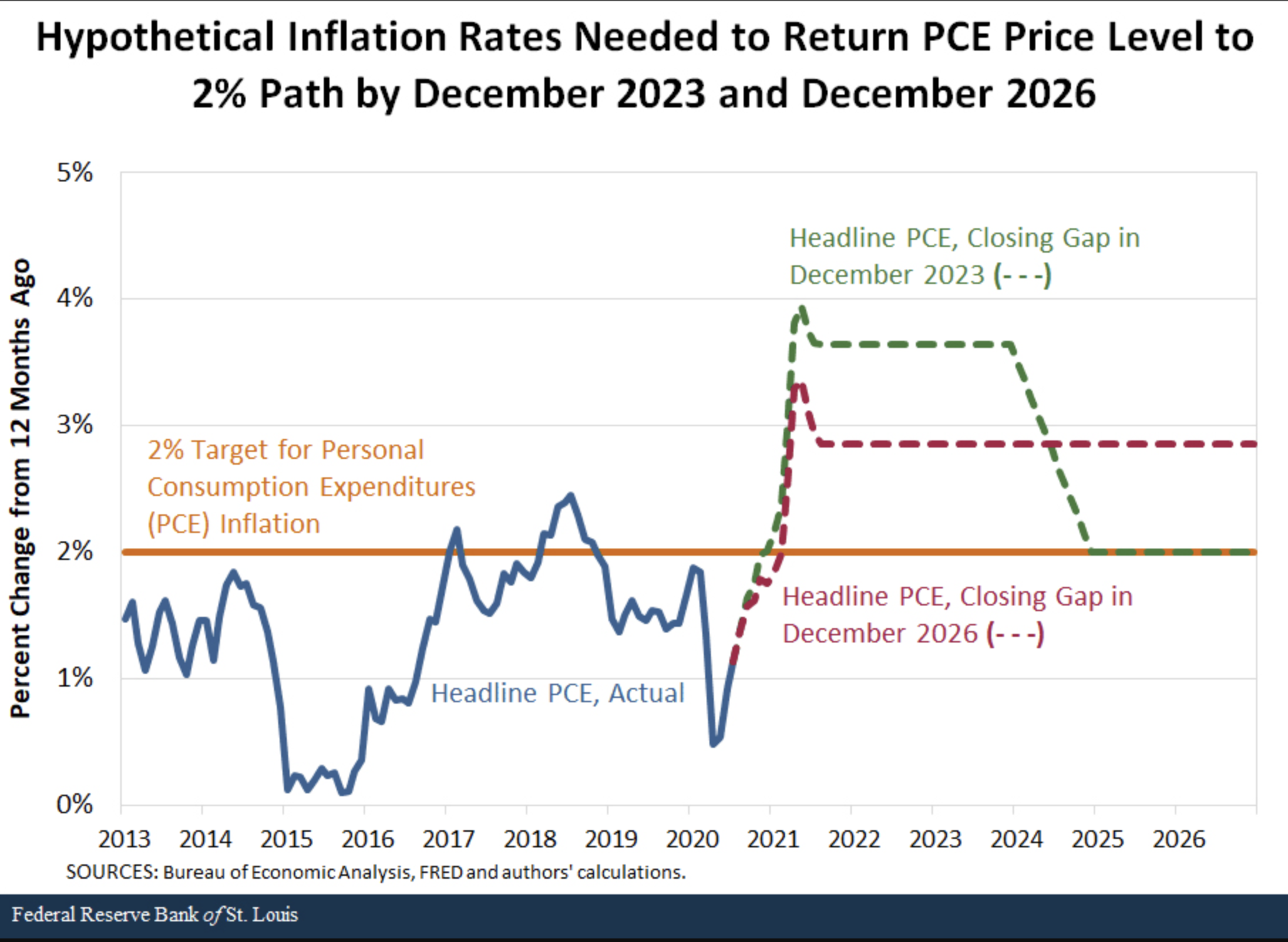

The Fed’s recent paradigm shift to sustain an average inflation rate of 2% implies that following periods where the inflation rate is under 2%, the Fed will have to raise the inflation rate above 2% for some period. As depicted in the graph below, the US ushered in an era of low inflation over the past decade up until recently when the economy rebounded from the pandemic. Hence, the question remains how much higher do inflation rates need to be in order to set the average inflation rate to 2%.

Image Source: Federal Reserve Bank of St. Louis

To illustrate this challenge, the graph depicts two hypothetical future scenarios the Fed could take to maintain an average 2% inflation rate. In the first scenario (green line), the inflation rate averages 3.6% per year from September 2020 to December 2023 in order to eventually return to an inflation rate of 2% by December 2024. In the second scenario (red line), the inflation rate averages 2.9% per year from September 2020 to December 2026 in order to eventually return to an inflation rate of 2% by December 2027 (Kliesen, Bokun). Regardless of the approach the Federal Reserve decides to take, it is safe to assume that the American and global economy will likely witness abnormally high inflation for years to come.

III. Previous Pandemic Measures to Protect Small Businesses

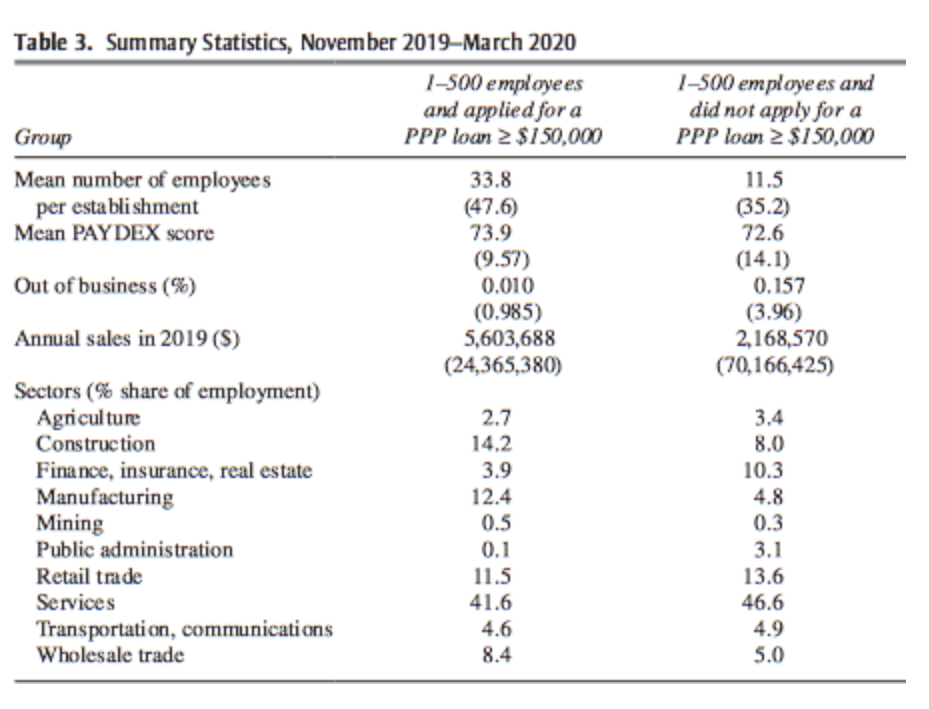

During the pandemic, the Small Business Administration (SBA) passed the Paycheck Protection Program (PPP) to provide loans that help small businesses fund payroll costs, employee benefits, rent, and utility costs. These loans had an interest rate of 1% with a maturity period of either two or five years depending on the issue date of the loan. However, small businesses could qualify for full loan forgiveness on the condition that employee and compensation levels are maintained, and at least 60% of the proceeds are spent on payroll costs. Under the PPP, the SBA released two separate waves of loans to small businesses until the program ultimately ended on May 31, 2021. The effects of the PPP can be examined through a study conducted by Hubbard and Strain, who utilized data from Dun & Bradstreet Corporation. The results of the study are depicted by the table below.

Image Source: Brookings

Image Source: Brookings

The table compares businesses with 1-500 employees that received a PPP loan of at least $150,000 relative to those that did not. As indicated by the table, businesses that received a loan experienced a 0.01% closure rate, while businesses that did not apply for a loan witnessed a 0.157% closure rate. Hence, it can be reasonably concluded that the PPP succeeded in helping businesses continue their operation expenses amidst the pandemic. Unfortunately, many of the pandemic’s effects on small businesses still linger, with 34% of small businesses remaining closed from COVID-19. Hence, it becomes necessary to examine solutions that bolsters small business growth.

IV. The Cancellation of Student Debt to Bolster Entrepreneurship

With millions of small businesses shutting down, revitalizing the presence of small businesses in America’s economy becomes crucial. One interesting policy proposal, which Senator Elizabeth Warren campaigned on, is the cancellation of student debt of up to $50,000 for approximately 42 million Americans. In 2021, outstanding student loan payments reached $1.7 trillion, which disproportionately burdens minorities. A study reports that twelve years after entering school, African American borrowers on average owe 114% of their loan, and Hispanic borrowers owe 79%, while white students owe 47%. Consequently, countless people, particularly minorities, become discouraged from obtaining the financing to start up their own businesses, a costly endeavor. The partial cancellation of student loans would serve as a catalyst for entrepreneurship and decrease racial disparities in entrepreneurship.

A lack of capital is a key barrier to entry for countless entrepreneurs. Statistically, at least 65% of entrepreneurs utilize personal and family savings to start their own business. However, people with student debt have to prioritize their savings to make monthly payments on loans, blocking them from financing a high-risk endeavor. Hence, the Federal Reserve of Philadelphia found that an 8% increase in total student debt in each county leads to 70 fewer new small businesses. On a micro level, Professor Krishnan from Northwestern University finds that a person with $30,000 in student loans (average debt at graduation) is 11% less likely to start a business than a person who graduated debt-free. Abolishing student loans would serve as a massive stimulus boost for countless middle class members – the drivers of small businesses – and lightens a weight that disproportionately prevents upward mobility for underrepresented communities.

This specific policy proposal of the cancellation of up to $50,000 in student debt lost traction because Senator Warren lost her presidential campaign. More broadly, student debt cancellation as an idea is still a politically challenging endeavor. For one, Republicans fully oppose the notion and many moderate Democrats remain less supportive, posing a major challenge for an evenly-divided senate. Another consideration is fairness; student debt cancellation would likely generate massive backlash from people who already paid their debts and people who never attended college. Outside of issues surrounding political feasibility, there are also additional considerations surrounding the efficacy of the policy itself. First, cancelling student loans can be seen as a band-aid solution that skims over the root issue: rising costs of higher education. The day after student debt is cancelled, more students will continue to line up for loans to fund their education, and student debt will eventually converge back to the original starting point. Hence, it would be reasonable to argue that student debt cancellation has no long-run significance absent additional measures to lower the costs of higher education. Finally, student loan cancellation is undoubtedly an expensive endeavor that could cost nearly $400 billion, a difficult pill to swallow for taxpayers.

V. Concluding Remarks

The US economy is largely shaped by small businesses – the driver of innovation, economic activity, and employment. Amidst the pandemic, millions of small businesses were forced to close because of safety protocols. Even as the economy reopens, small businesses remain in a tough predicament due to supply chain disruptions and rising wage costs. Hence, revitalizing entrepreneurship to expand the presence of small businesses should be a high legislative priority. One unorthodox solution to accomplish this is mitigating student debt, which provides the necessary fiscal stimulus to millions of people to finance their own businesses. In addition to increasing economic output, the cancellation of student debt would enhance the equity of our society by abolishing an issue that disproportionately impacts underrepresented communities.

Featured Image Source: The North Bay Business Journal

Disclaimer: The views published in this journal are those of the individual authors or speakers and do not necessarily reflect the position or policy of Berkeley Economic Review staff, the Undergraduate Economics Association, the UC Berkeley Economics Department and faculty, or the University of California, Berkeley in general.